Speaking exclusively to Quarrying Africa, Snyman says although the South African construction industry experienced another difficult and challenging year in 2023, turnover in the sector recorded a moderate 4% growth for the first three quarters, recovering from a 10% decline in nominal terms in 2022. This is according to Stats SA’s quarterly financial statistics, which somehow differs from the gross capital formation estimates that have shown an average increase of between 8% and 9% in 2022 and 2023 (first three quarters).

Snyman notes that gross fixed capital formation estimates entail a broader definition for construction, and that includes machinery and equipment used in the sector. To provide context, actual turnover in construction was around R95-billion lower compared to gross fixed capital for the sector (including construction works, residential and non-residential investment). With the rapid growth in renewable energy projects, Snyman notes that the impact of imported machinery and equipment is more profound on official investment estimates and can be misleading.

Sector performance

Commenting on sector performance in 2023, Snyman says residential construction growth slowed to 5% year-on-year (YoY) in the first three quarters, following a double digit increase during 2022, whereas non-residential investment growth accelerated from 2% to 11% YoY, during the same period.

“It must be noted, however, that investment growth in the non-residential market is coming off a dismally low base, as private sector demand in this sector has declined substantially over the last few years,” she says. “There was around R8-billion more invested in buildings up to September 2023, with R11-billion added to construction works, representing a nominal increase of 9%.”

The construction labour force reacted positively to the moderate increase in investment, and expanded by an average of 116 000 work opportunities, or 10%, recovering to 2018 levels in the process and even surpassing pre-Covid levels.

“Some provinces significantly outperformed others, with the construction labour force in the Western Cape reaching record high levels and Northern Cape, albeit a smaller province in economic and construction terms, coming close to breaching its own record. Several other provinces have exceeded their long-term average, including KwaZulu-Natal, North West, Mpumalanga and Limpopo,” says Snyman.

Margins were also better, with contractor profitability improving to an average of 5% by the end of September 2023, compared to an average of 2,4% in 2022, although larger contractors are still underperforming against the industry average, with an average margin of around 3%. Although confidence amongst building and civil contractors reached its highest level since 2017, Snyman says the majority of contractors are still feeling rather pessimistic.

It was a difficult year for the listed construction sector companies, as average market capitalisation values declined by an average of 22% YoY for retailers and contractors, and around 2% for construction material suppliers such as Afrimat, PPC and Sephaku.

Interestingly, the cumulative market capitalisation of retailers in construction (including Cashbuild and Italtile) represented only 7% of the total market capitalisation values of contractors in 2008, but was 14% higher by comparison in 2023, as contractors lost 80% since 2008 (excluding Group Five and Basil Read). On the other hand, Wilson Bayle Holmes and Stefanutti Stocks outperformed the average, with average market cap values up by between 42% and 66% compared to 2022. Afrimat bucked the trend in terms of suppliers, while Cashbuild and Italtile both recorded weaker values on average in 2023.

Improved outlook?

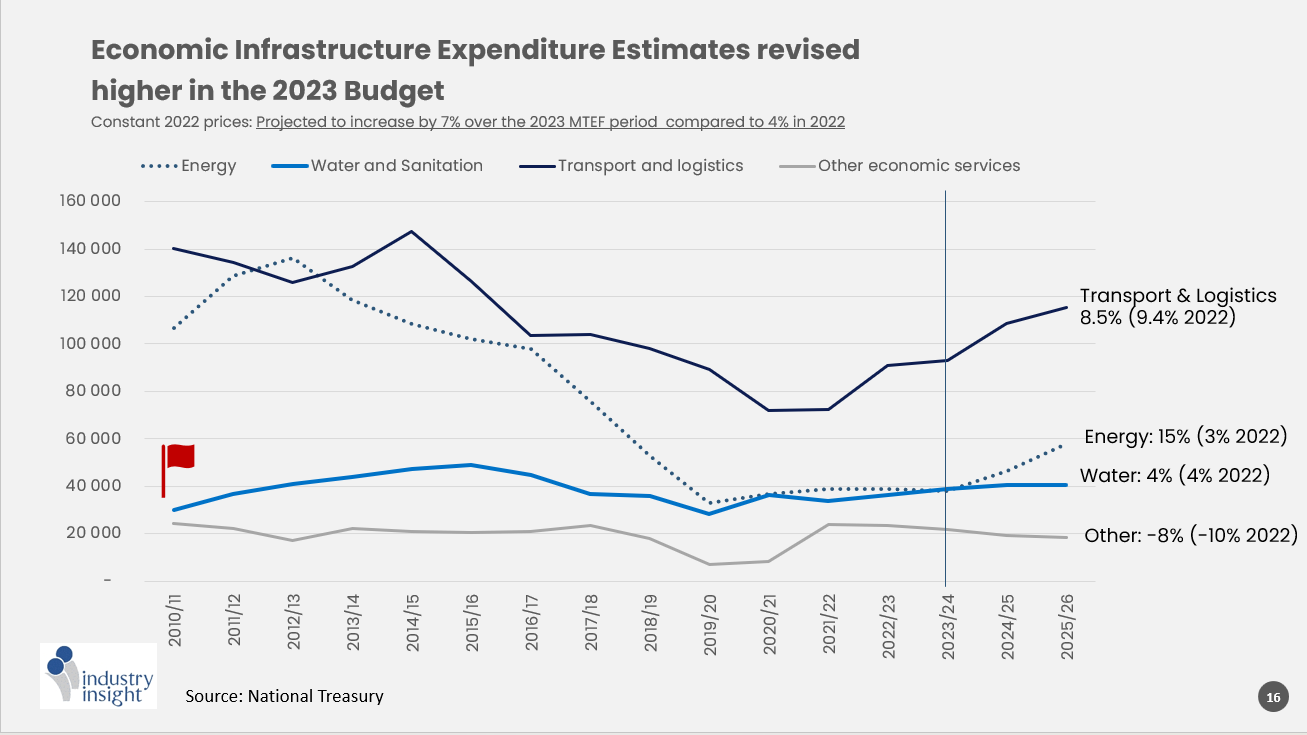

If infrastructure expenditure is anything to go by, then, says Snyman, the outlook of the construction sector has certainly improved. However, she says, this largely relates to economic infrastructure, or civil construction. Investment in the civil sector is largely public sector-driven, and with anticipated higher levels of investment coming from the private sector, that will add more impetus for improved growth rates in the sector.

“On average, President Ramaphosa has mentioned infrastructure in his State of the Nation Address (SONA), 66% more times during this four-year tenure than Jacob Zuma did during his entire tenure. The 2023 SONA alone referred to infrastructure a record number of 22 times since the 1994 SONA. This shows that the need for infrastructure expenditure has clearly become a national priority,” says Snyman.

Sadly, adds Snyman, infrastructure was not as prominent in the 2024 address compared to 2023. This, she says, does not mean however, that the Budget for 2024 will be reprioritised lower, as the momentum set in 2022 and 2023 should filter through to higher infrastructure expenditure. The question is whether the momentum will be sustained for at least the next three to five years, or even post-election.

The focus is largely to mitigate the current crises in energy, transport and logistics, as this has had the direst economic impact, which means, concerningly, there is less focus on social infrastructure expenditure (housing, education and health). So, she says, there is not much expected in terms of government support in investment in buildings. This will see continued pressure on investment in buildings following last year’s contraction.

To provide context, private sector demand for buildings deteriorated in 2023, with approvals for new construction work down 16% YoY in the 12-months up to November 2023 (measured in square metres). The residential sector was particularly hard-hit, with approvals declining by 21%. However, Snyman notes that there is some momentum in terms of commercial office space approvals, coming off a dismally low base, with approvals up 26% by November 2023, support also coming from retail space (up 4%) and renovations recording a second year of double-digit growth.

The industrial sector, previously the star performer in the non-residential space, is much weaker, with approvals declining by 16% in 2023. While there may be pockets of growth, the overall impact at a national level is weaker expected investment into the non-residential sector, aggravated by declining demand in the residential market.

Investment in buildings has shown no recovery since Covid hit in 2020, and with heightened political uncertainty, the impact of higher interest rates along with dismal economic performance, it seems unlikely that the building industry will recover any time soon.

“On the upside, we may have reached the turning point in terms of interest rates, with a broad consensus that interest rates will start to ease at a moderate pace in the second half of 2024, hoping to reach normality (around 10%) by the end of 2025,” she says.

Tender activity

Economic growth forecasts remain weak, however, with most projections not expecting economic growth to breach 2% in the next three years; previous forecasts of around 1,5% for 2024 have already been revised lower, to around 1%, given the state of key institutions such as Eskom and Transnet.

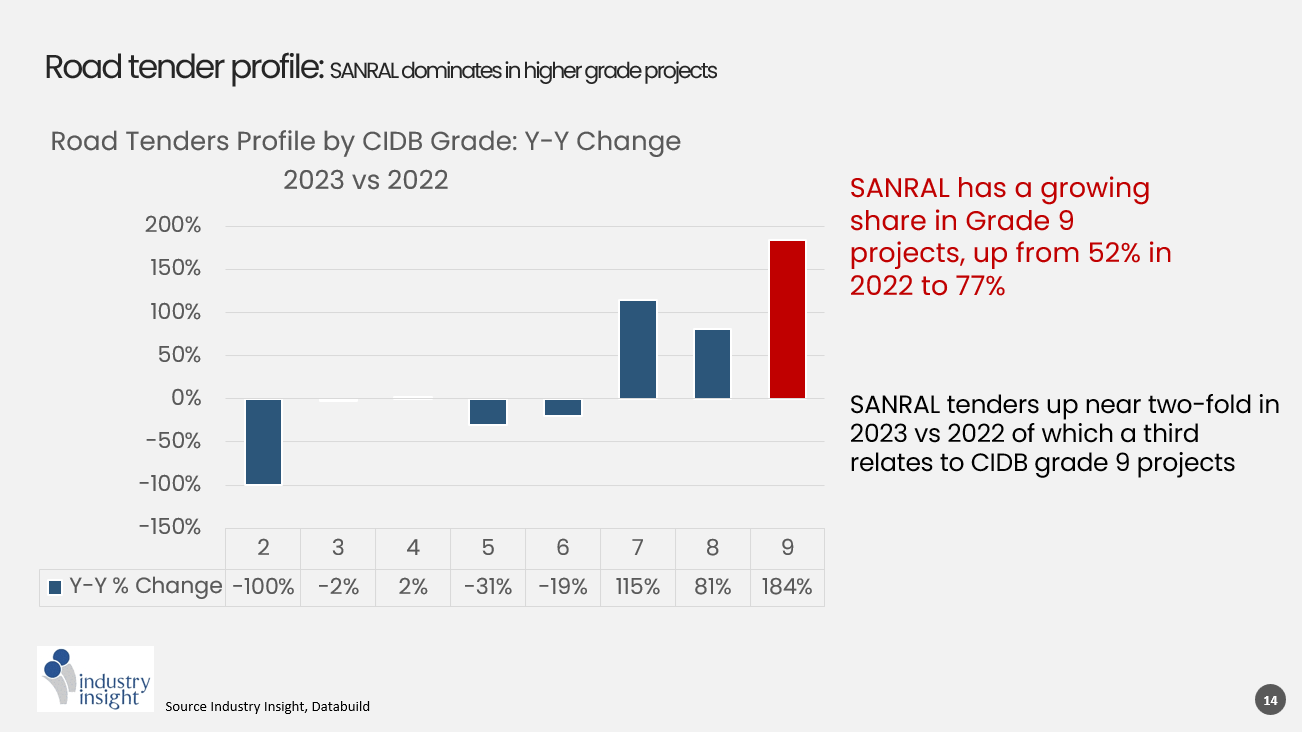

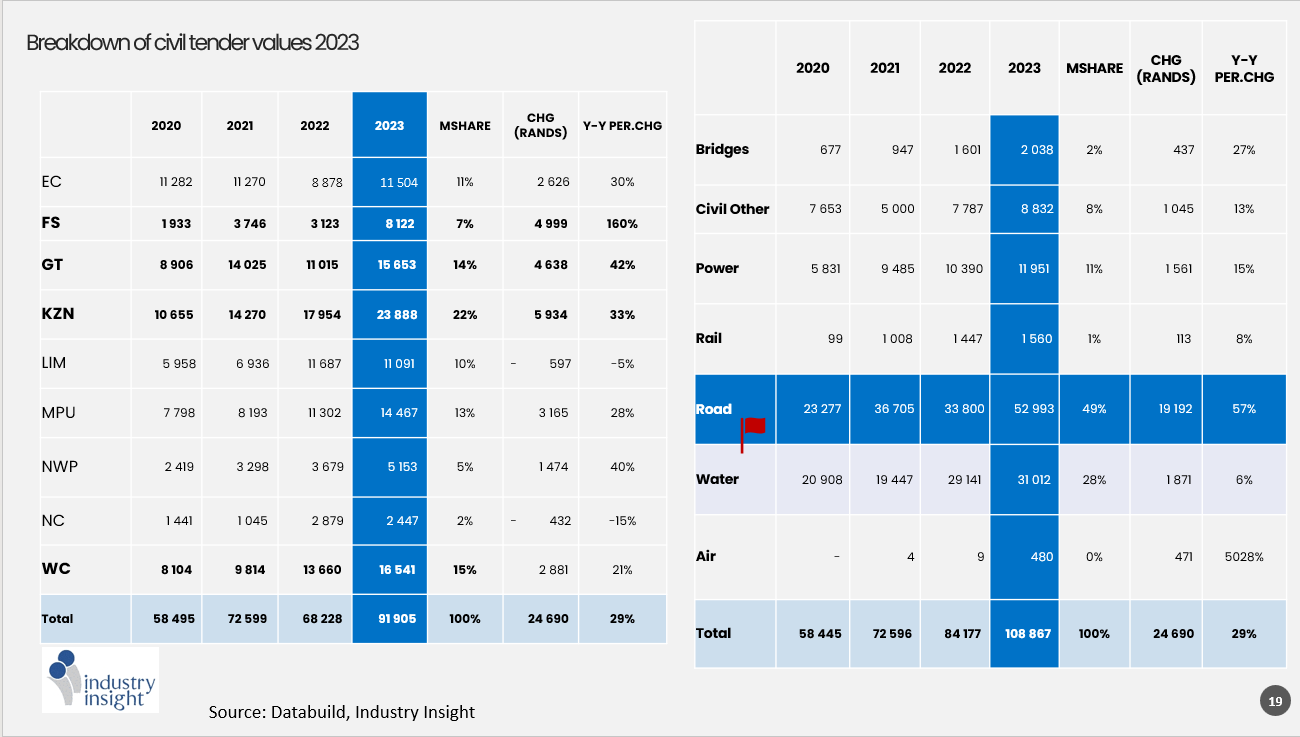

“What we have seen, however, is a rather robust increase in civil tender activity, with the estimated nominal rand value of civil tenders up 29% YoY in 2023, with most of the provinces showing an increase compared to 2022,” says Snyman. “The estimated value of road tenders rose 60%, with SANRAL a major contributing client.”

Tender activity, she says, generally accelerates in the run-up to an election year, as evidence has shown historically, so one cannot help but be concerned that the current momentum in tender activity is going to slow down post-election (as it almost always does). The awarding of contracts has also been a problem, but there seems to have been some progress in 2023, as the pace of awards in civil tenders has improved. The big question, says Snyman, is around sustainability of this momentum and the infrastructure expenditure estimates projected for the next three years.

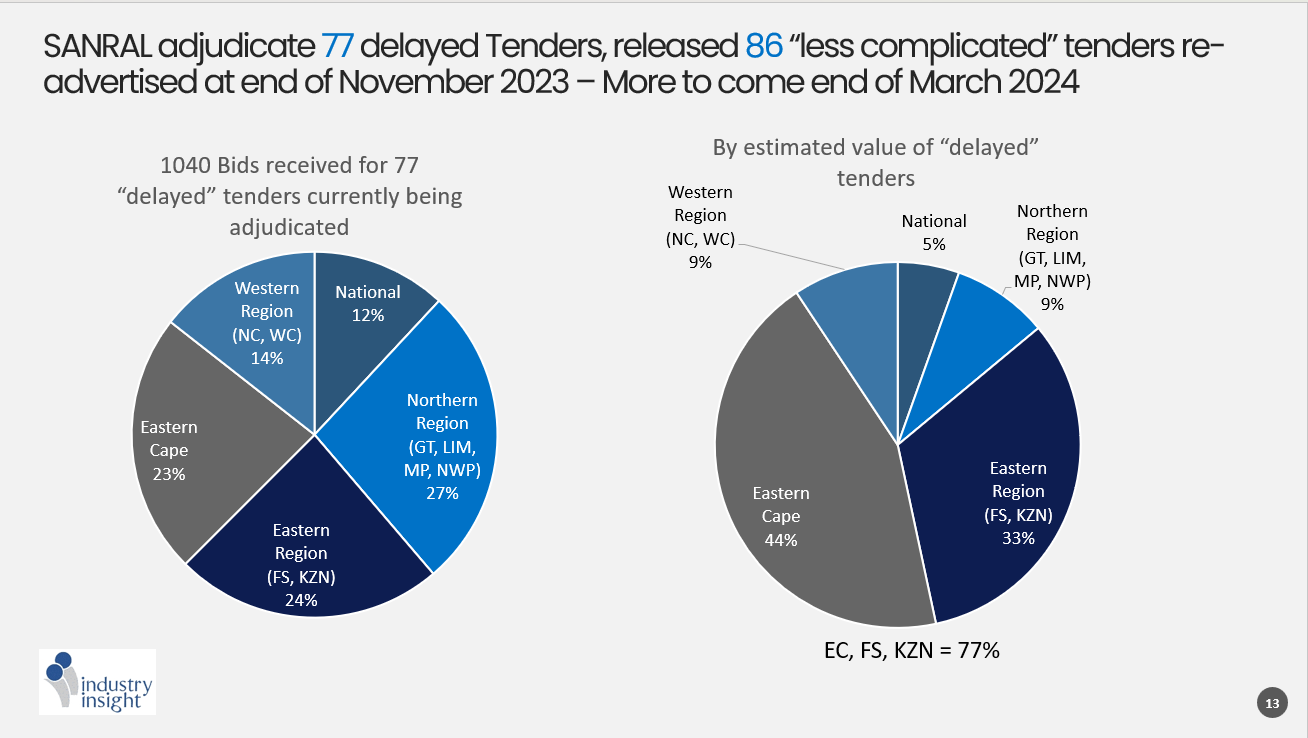

“SANRAL is the most prominent current player in the road sector, and any delays to tender adjudication has a significant impact on the industry. It is therefore imperative that any unnecessary delays, as experienced in 2023, are prevented in the future. Uncertainties created by the Public Procurement Bill, passed in December 2023, have severely impacted the construction sector, with multibillion-rand projects being delayed by a wave of court interdicts that could have been prevented,” she says.

SANRAL has a significant footprint across all provinces, where it remains the dominant player in road construction, except in the Western Cape. The total number of road contracts out to tender increased by 11% YoY in 2023, with an increase of 66% from SANRAL. All in all, despite the delays, conditions for the road segment have improved.

Trends

Commenting on some trends in the market, Snyman says a few things are at play that could ultimately transform the construction landscape. Of note is the increasing role of the private sector in economic infrastructure development. The result is a rather robust expansion of public-private partnerships (PPPs), which is currently taking place at an unprecedented level.

The upside of a broad-based infrastructure collapse that is having a debilitating impact on the economy, is the acceleration of privatisation as government scampers to find appropriate and ‘fast’ solutions to the economic crisis. For now, she says, this is still very much focused on energy distribution, but the platform for greater participation in transport and even water services is being laid.

“We have already seen an increase in the announcement of large scale, or high economic impact, PPP projects in 2023, expected to filter through even to local government level. Developmental plans associated with green hydrogen are also moving at a faster than expected pace and can transform the provincial landscape for provinces such as the Northern and Eastern Cape,” says Snyman.

Part of this privatisation process is to streamline the regulatory framework and to bring greater consistency within the various policy frameworks, in order to reduce uncertainties. Business confidence remains depressed, however, given the fact that corruption in South Africa is not by any means perceived to be under control, with the construction mafia still overpowering many projects across the country.

“I must say, however, that I feel there is a fundamental shift presently taking place, where government and the private sector can finally take hands and share the developmental responsibility so desperately needed for the country. 2024 is likely to remain another challenging year, with the IMF’s latest economic forecast for South Africa having been revised lower to just 1% and the impact of higher lending rates on consumers still rippling through the economy, and expected to continue to do so for at least the next two years,” she says.

In conclusion, Snyman says the biggest wildcard is the 2024 National Election (one of many across the world) that may result in weaker tender activity, directly impacting the construction sector, where political appointments are affected, or even potentially, a complete revision of the country’s economic policy. The local construction sector almost always pays the price for these political changes, especially at local government level.