The significance of the construction sector to any economy cannot be emphasised enough. By creating jobs, stimulating investment, improving infrastructure, contributing significantly to gross domestic product (GDP) and facilitating economic growth through its intersectoral linkages with other industries, construction is the physical foundation needed for the economy to thrive.

Despite significant challenges in recent years, the South African construction industry remains a critical pillar of the domestic economy, contributing 5% to the nation’s GDP in expenditure terms, with a labour force exceeding 1,3-million as of the third quarter of 2024.

Notably, the sector has a high employment multiplier effect – for every R1-million invested, it generates employment for more than four individuals, and this figure rises to an estimated nine jobs when including associated roles in the material manufacturing sector. These figures, says Snyman, underscore the industry’s significant role in both economic output and job creation within South Africa.

State of affairs

After enjoying an historic growth phase during the run-up to the 2010 Soccer World Cup, the South African construction industry has generally withstood a rocky period during the past decade. Despite substantial investments in renewable energy and a political push to enhance infrastructure ahead of the May 2024 elections, the performance in building and construction remained weak, with the construction sector experiencing an 8% year-on-year decline in investment during the first three quarters of 2024, following a 3,7% contraction in 2023. Factors such as higher interest rates, increased inflation and political uncertainties were key constraints to private sector investment, a key driver in the building sector.

The challenges were not only unique to the building sector, with the civil construction segment also facing difficulties, with a 7,6% year-on-year decline in investment during the same period. However, confidence among civil contractors rebounded in the latter half of 2024, attributed to government efforts to boost infrastructure spending.

“The civil industry presented a mixed scenario, with weak investment growth alongside improved confidence. Investment in construction works fell by 1,7% year-on-year in 2023, which accelerated to a 7,6% year-on-year decline in the first three quarters of 2024. Yet, confidence levels among civil contractors showed a notable rebound during the second half of 2024, reaching an eight-year high of 50 in the third quarter of 2024, according to the FMB/BER Confidence surveys,” says Snyman. This follows a concerted effort by the government, prior to the May 2024 elections, to increase infrastructure expenditure, given the debilitating economic impact of failed economic infrastructure deeply entrenched across all government spheres.

Spending priorities

Despite these initiatives, the reallocation of funds in the 2024 Budget from transport and energy to water services, coupled with a decline in social infrastructure expenditure, has raised concerns about the government’s investment strategy.

“Infrastructure spending priorities announced in the 2023 Budget, which included the 2023/24 financial period, suggested higher levels of investment in the transport and energy sectors, with an encouraging overall real increase of 4,5% projected over the Medium-Term Expenditure Framework (MTEF) period (2023/24 to 2025/26),” says Snyman.

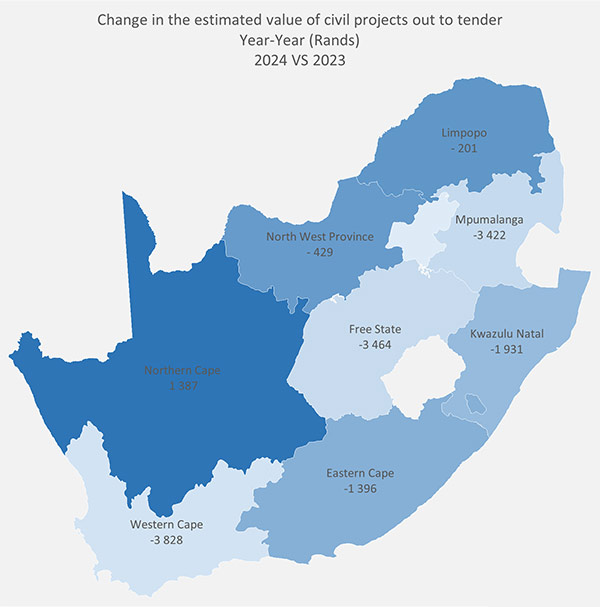

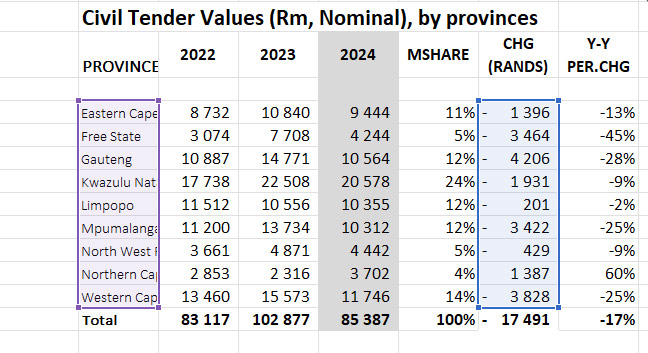

“We also observed an 11% year-on-year increase in public sector civil tender activity during the first six months of 2024, compared to the same period in 2023. However, this was followed by a post-election slump, as tender activity fell by 17% year-on-year during the second half of 2024,” she adds.

In the 2024 Budget, the government reallocated infrastructure funding, shifting focus from transport and energy sectors towards water services. This shift coincided with a continued real decline in social infrastructure expenditure estimates, notably in housing, education and health sectors.

Overall, projections for total public sector infrastructure expenditure indicate an average 0,1% decline in real terms over the MTEF period up to 2026/27, suggesting a governmental approach contrary to widely advocated investment strategies.

Key challenges

The industry, says Snyman, continues to grapple with challenges such as intimidation from groups known as the “Construction Mafia”, corruption, project cancellations and payment delays. In 2024, project postponements increased by 27% year-on-year, affecting over 200 projects, while cancellations rose by 82%, impacting 344 projects, as reported by industry sources such as Databuild. Profit margins also declined, averaging less than 2% up to the third quarter of 2024, down from 5,2% in 2023, primarily due to intensified competition.

The decline in public sector tender activity in both building and civil sectors during the latter half of 2024 may adversely affect turnover in the short to medium term. The extent of this impact will largely depend on how swiftly the new Government of National Unity (GNU) can rejuvenate tender processes, particularly at provincial and local government levels. Early 2025 has seen increased friction within the GNU, linked to the signing of the Expropriation Act in January 2025. This development has the potential to undermine investor confidence, thereby slowing private sector investment.

In addition, the manufacturing sector in South Africa is grappling with numerous challenges, including escalating input costs, logistical constraints and the threat of imports, all of which adversely affect suppliers of construction materials. A prominent example is ArcelorMittal South Africa’s recent announcement to wind down its long-steel operations, a decision expected to impact approximately 3 500 direct and indirect jobs.

The local cement manufacturing industry faces similar hurdles. Cement imports increased by nearly 20% in 2023, reaching 979 000 tonnes, with a notable 43% year-on-year growth in the second half of the year.

“The surge in cement imports poses a significant threat to domestic cement producers, who are already contending with higher input costs and logistical challenges. These developments underscore the pressing need for strategic interventions to bolster the competitiveness of South Africa’s manufacturing sector and safeguard its role in the country’s infrastructure development initiatives,” notes Snyman.

A few bright spots

Despite these challenges, sentiment towards the listed construction sector improved during the latter part of 2024. Notably, cumulative market capitalisation values increased by 76% year-on-year in the second half of 2024, indicating renewed investor confidence in the sector.

“On a more positive note, building approvals for new private sector construction appear to have reached a low point, with demand for non-residential buildings and housing gradually improving towards the end of 2024. This trend is partly attributed to a more favourable interest rate environment. However, considering that project approvals typically have a lead time of 12 to 18 months, the building sector may continue to face challenges at the start of 2025,” says Snyman.

The outlook for further interest rate cuts in 2025 has become more uncertain due to renewed global economic uncertainties. Following three consecutive cuts, the South African Reserve Bank reduced the key interest rate to 7,5% on January 30, 2025. While further reductions are anticipated throughout the year, with projections suggesting a rate of approximately 7,25% by year-end, these expectations are contingent upon the absence of unforeseen economic shocks.

Unlocking investment

Commenting on what needs to be done, Snyman says, to address the significant fiscal challenges and reduce escalating debt levels, increasing private sector investment is essential.

“This will require bold actions by the government to restore investor confidence, reduce regulatory obstacles and create a conducive environment for private sector participation. Despite over R658-billion in new project announcements in 2024, the uptake has been slow, indicating the need for effective implementation strategies,” she concludes.